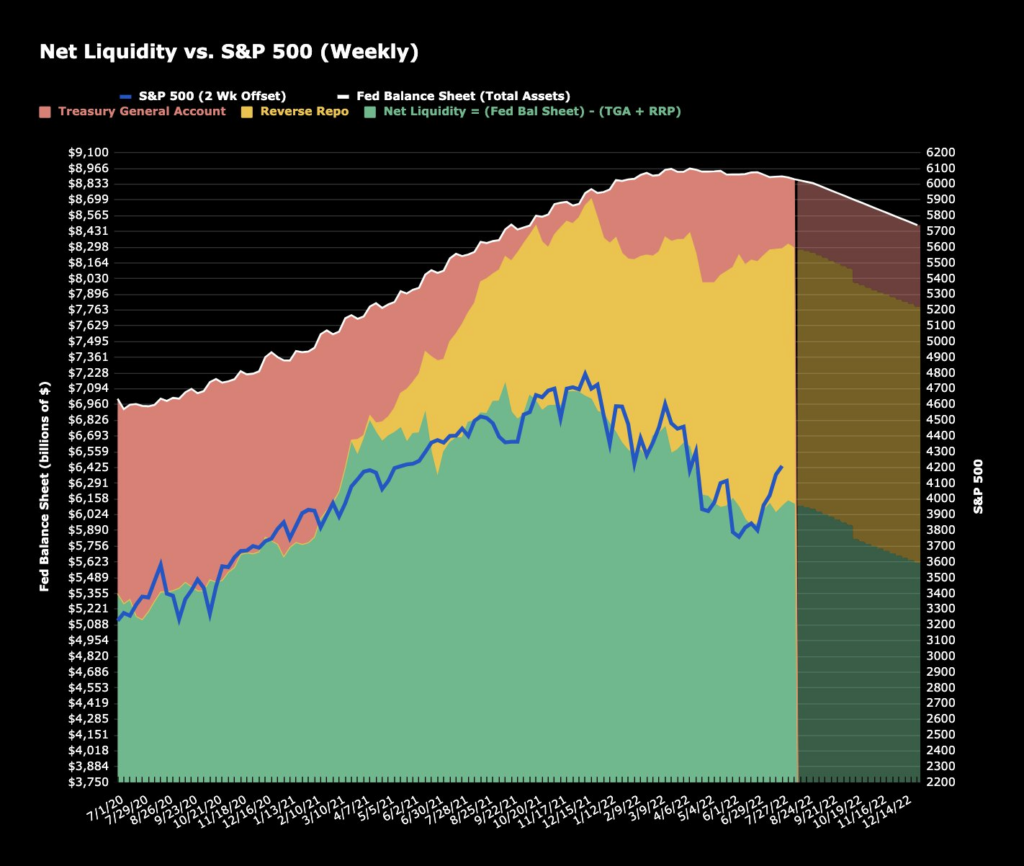

Mind The (Liquidity) GAP

Since early July we have seen every pullback in the US Markets hold above support and then push higher resulting in the upward chop to new highs week after week. The liquidity landscape has been hugely supportive during this period leaving Primary Dealers flush and markets buoyed.

Taking stock and looking forward over the coming weeks and months things may not be so straight forward (or “upward”) from here.

We are aware that the US Treasury has built up a considerable cash balance over recent months, That currently stands at circa $1.7 Trillion. According the FOMC minutes from last week the FED has also stated that it intends to continue its current regime over the next quarter and indeed for the foreseeable future.

This week, the Treasury Borrowing Advisory Committee (TBAC) issued its quarterly re funding report. This can of course be revised but even taken at face value the numbers are going to put some serious pressure on the overall liquidity scenarios over coming months. The US Treasury intends to sell $172 Billion of paper in August followed by a further $218 Billion in September. Add to that an estimated $540 Billion in T-Bills (Bonds) from mid August onwards, which distributed evenly suggests around $75 Billion per week.

The US Treasury has already got $62 Billion in notes & bonds that it intends to issue on 17th August. Adding all this together we can surmise that the total in new debt between now and the end of the month comes to a cool $324 Billion. That is mostly loaded into the weeks following the 17 -20th August.

Going back to the FED and their “Stay calm & Carry On” approach. They are committed to purchase $80 Billion per month in Treasury purchases. $40 Billion per month in Mortgage Backed Securities (MBS) at the same time as purchasing enough MBS each month to replace those that it holds that are being prepaid. These settle during the third week of each month and total $116 Billion in August. All of those purchases equate to more cash to the Primary Dealers so are potentially positive for the markets.

So the liquidity equation from 17-20th August through to the end of the month looks like this.

New Treasury Supply (Negative) $324.00 Billion

FED QE $40 B + $116 B ( Positive) $156 Billion.

As the saying goes:

“ Annual income twenty pound, annual expenditure nineteen six, result happiness

Annual Income twenty pounds, annual expenditure twenty pound ought and six, result misery”

Charles Dickens, David Copperfield

So that looks like $168 Billion of Dickension misery headed the Markets way from around the third week of the month.